Most people have a rough sense of whether money feels tight or comfortable — but a rough sense is not the same as knowing. This guide walks you through a structured, honest self-assessment so you can compare your actual income against the living wage for your specific location and household situation. No guessing. No national averages. Just a clear answer to the question most people are too anxious to sit down and work out properly.

What This Guide Covers

Work through each section in order, or jump to what you need.

Why Knowing Matters — Even When the Answer Is Uncomfortable

There is a particular kind of financial anxiety that comes not from knowing your situation is bad, but from not knowing exactly how bad — or whether it is actually bad at all. A lot of people live in that ambiguous middle space. They feel stretched but aren’t sure if the feeling is accurate or if they are just bad at managing money. They wonder if their salary is actually reasonable for where they live, or whether everyone around them is quietly struggling the same way.

The living wage assessment does not solve any of those problems on its own. But it does something more valuable than comfort: it replaces ambiguity with clarity. You get a number. Your income either clears it or it doesn’t. The gap, if there is one, is a specific dollar amount — not a vague sense of unease.

That clarity changes what you can do next. If you are above the living wage, you know your baseline is covered and you can focus on the goals above it — savings, debt repayment, building a cushion. If you are below it, you know the problem is structural — not a personal failing or a discipline issue — and you can start looking at it like a problem to solve rather than a character flaw to be ashamed of.

Neither answer is comfortable. But both are more useful than not knowing.

This assessment builds on the living wage figure for your specific county and household type. Pull that number now from the MIT Living Wage Calculator on Waldev — it takes about 60 seconds and is the foundation everything else here depends on.

Before You Start: What the Living Wage Does Not Measure

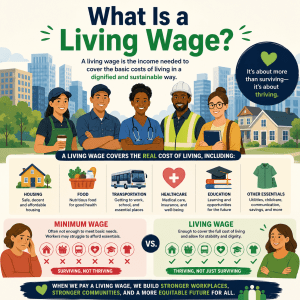

Running this assessment honestly requires understanding what the living wage benchmark includes and — just as importantly — what it leaves out. People sometimes get a confusing result because they expect the living wage to account for things it deliberately does not.

✅ What the living wage covers

- Market-rate rent for a basic unit appropriate for your household size

- Groceries based on the USDA low-cost food plan (home cooking, no dining out)

- Basic transportation — a car in most counties, transit where available

- A basic employer-sponsored health insurance plan

- Center-based childcare for children in your household (if applicable)

- Basic personal care and household supplies

- Federal, state, and payroll taxes on the gross income required

❌ What the living wage does NOT cover

- Student loan or other debt repayments

- Emergency fund contributions

- Retirement savings or pension contributions

- Dining out, entertainment, or holidays

- Home ownership costs

- Life or disability insurance premiums

- Any meaningful discretionary spending

- Savings goals of any kind

This matters because it reframes what it means to “pass” the living wage check. Clearing the threshold does not mean you are financially comfortable. It means your most basic expenses are technically covered by your income. Everything above that — savings, debt repayment, financial security — requires earning above the living wage, sometimes considerably above it.

⚠️ If you carry significant debt: The living wage calculation does not include debt repayment. If you have student loans, credit card balances, or a car loan, your effective income requirement is higher than the living wage figure suggests. We address this separately in the debt section below.

Step 1 — Find Your Living Wage Baseline

The living wage is not a national number you can look up once and apply everywhere. It varies county by county, driven by local housing costs, childcare prices, and transportation needs. The figure you need is the one for your specific county and your specific household situation.

Open the free MIT Living Wage Calculator on Waldev. You do not need to create an account or provide any personal details. The tool is completely open.

Choose the state where you currently live, then select your specific county. If you live in a major metro area, make sure you select the county, not just the city — living wages can vary significantly even between neighboring counties in the same metro area.

The calculator shows living wages for several household configurations. Identify the one that matches your actual situation — single adult, single parent with one child, two adults both working, two adults one working with children, and so on. Choose the configuration that reflects how your household is actually structured right now, not how you wish it were.

Note the hourly living wage for your household type. To get the annual equivalent, multiply by 2,080 (the standard number of work hours in a full-time year: 40 hours × 52 weeks). Write both numbers down — you will use them in the next steps.

Your living wage (annual equivalent)

Living wage (hourly) × 2,080 = Annual living wage income needed

💡 Multi-county households: If you and your partner work in different counties, or if you are considering a move, run the calculator for each relevant county separately. The figure can shift meaningfully even across short distances, particularly where housing markets have sharp edges between jurisdictions.

Step 2 — Calculate Your True Hourly Rate

The living wage is expressed as a gross hourly figure. To make a fair comparison, you need to convert your own income to the same format. This is where a lot of people get tripped up — they compare a vague sense of their annual salary against the living wage without doing the actual conversion, and end up with an imprecise answer.

Work through the relevant calculation below for your income type.

If you are salaried

Salaried worker — hourly equivalent

Annual gross salary ÷ 2,080 = Your effective hourly rate

Example: $52,000 ÷ 2,080 = $25.00/hour gross

If you are hourly

You likely already know your hourly rate. Confirm that the figure you are using is your gross rate — what you earn before tax deductions. If you earn a different rate for overtime, use your standard rate for this calculation. Overtime is not guaranteed income and should not be used to inflate the comparison.

If you have variable or multiple income sources

Variable / multiple income sources

Add all gross income sources for the past 12 months

(Primary job + side income + freelance + any other regular income)

Total annual gross income ÷ 2,080 = Effective hourly rate

Note: Use 12-month actuals, not projections. Be conservative.

⚠️ Use gross income, not take-home pay. The living wage figure is a gross income benchmark — it accounts for taxes within the calculation. If you compare your net (after-tax) take-home pay against the living wage, you will appear to fall short even if you actually meet the threshold. Always use gross figures on both sides of the comparison.

Step 3 — Match Your Household Type Correctly

This step catches more errors than any other. People frequently compare their individual income against the wrong household type — usually the single adult figure — when their actual household structure requires a different benchmark. Getting this wrong gives you an answer that is too optimistic or too pessimistic.

| Your actual situation | Which household type to use | Compare against |

|---|---|---|

| You live alone, no children, no dependents | 1 adult, 0 children | Your individual hourly rate vs. the single adult living wage |

| You and a partner both work, no children | 2 adults, 2 working, 0 children | Each person’s hourly rate vs. the per-adult living wage for that household type |

| You and a partner, only you work, no children | 2 adults, 1 working, 0 children | Your individual hourly rate vs. the full household living wage (one earner covers it all) |

| You are a single parent with one child | 1 adult, 1 child, 1 working | Your individual hourly rate vs. the single parent living wage — this will be significantly higher than the childless single adult figure |

| You and a partner both work, two children | 2 adults, 2 working, 2 children | Each person’s hourly rate vs. the per-adult living wage for that configuration |

| You and a partner, only one works, two children | 2 adults, 1 working, 2 children | The working partner’s hourly rate vs. the full household living wage — this is typically the highest requirement of any common household type |

💡 If your situation is mid-transition — say, your partner has recently stopped working or a child was just born — run the calculation for both your old and new household type. The gap between those two figures shows you exactly what the life change has done to your required income, and how large a new financial challenge you may be navigating.

Step 4 — Account for Benefits That Offset Living Costs

The living wage calculation assumes a worker receives no employer benefits — all costs come out of wages. In reality, benefits can meaningfully change the picture. If your employer provides health insurance, contributes to childcare costs, or offers free transit, those benefits are reducing your out-of-pocket exposure in categories the living wage calculation includes.

This step is about being honest, not generous. Only count benefits that genuinely reduce a cost category the living wage covers, and only count them at their real market value.

Employer health insurance contribution — Healthcare is a direct living wage cost component. Find out how much your employer pays toward your monthly premium. If your employer covers $400/month and you pay $150, the employer contribution is $4,800/year in effective compensation that reduces your required gross income. Divide by 2,080 to get the hourly equivalent: roughly $2.31/hour in this example.

Employer childcare assistance — If your employer offers a Dependent Care FSA contribution, on-site childcare, or childcare reimbursement, these reduce a cost that sits directly in the living wage calculation for households with children. Value them at what they actually save you annually.

Transit pass or commuter benefit — Transportation is a living wage component. If your employer provides a transit pass or pre-tax commuter benefit, calculate its annual value and divide by 2,080 to find the hourly equivalent.

Employer meal provision — Food is a living wage component. If your employer provides free or subsidised meals, estimate the annual value honestly — not the retail value of fancy catering, but what you actually save on grocery or meal costs.

Add up the hourly equivalents of all genuine benefits in the above categories. This is your effective hourly compensation — your base wage plus the value of relevant benefits. This is the figure that more accurately represents your real economic position relative to the living wage.

Effective hourly compensation

Base hourly rate + (Annual benefit value ÷ 2,080) = Effective hourly rate

Example: $22.00 base + ($4,800 health contribution ÷ 2,080)

= $22.00 + $2.31 = $24.31 effective hourly rate

⚠️ Only count benefits that actually reduce a living wage cost category. Retirement match, stock options, gym memberships, and professional development stipends are valuable — but they do not reduce the costs the living wage covers. Counting them here inflates your result and gives you a falsely optimistic picture.

Step 5 — Calculate Your Gap or Margin

This is the moment of clarity. With your effective hourly rate and your local living wage figure both in front of you, the calculation is simple.

Your living wage gap or margin

Your effective hourly rate − Living wage for your county and household type

Positive result = You are above the living wage by this amount per hour

Negative result = You are below the living wage by this amount per hour

Annual equivalent: Gap/margin (hourly) × 2,080

Work through it with your own numbers using the worksheet below.

Multiply line E by 2,080 to see the annual equivalent of your margin or gap. That figure — in annual dollars — is often the most emotionally legible way to understand the result. A $3/hour gap sounds abstract. A $6,240 annual shortfall feels real.

What Your Result Actually Means

The number you have calculated places you in one of four zones. Here is what each one means in practical terms — honestly, without sugarcoating the difficult ones.

Below the living wage — a meaningful gap

Your income, including relevant benefits, is not sufficient to cover basic living expenses in your location for your household type. This does not mean you are failing — it means the income structure you are working within has a real mathematical shortfall. Most people in this zone are managing through some combination of debt, assistance programs, a second income, shared housing, or cutting costs in ways that create risk. The gap is structural, not personal. But it needs to be addressed because it tends to compound over time. Skip to the If You Are Below section for specific next steps.

At or just above the living wage — technically covered, no cushion

Your income covers your basic expenses — or just barely clears them. This is the most deceptive zone. You might feel like everything is fine because the bills get paid, but there is almost no margin. A single unexpected expense — a car repair, an emergency room visit, a rent increase — can tip you from technically covered into genuine hardship very quickly. The living wage is a floor, not a comfortable income. Being just above it means you are standing on that floor with nothing underneath you if you step off.

Comfortably above the living wage — financial margin exists

Your income exceeds your basic needs by a meaningful amount. This is real financial breathing room — enough to build an emergency fund, contribute to retirement, manage unexpected costs without going into debt, and work toward financial goals beyond mere survival. Being here does not mean you are wealthy or that money is no object. But it does mean the structural foundation is solid. Your focus can shift from survival to building. Skip to the If You Are Above section for what to focus on next.

Well above the living wage — building genuine security

You have significant margin above your basic expense floor. This puts you in a position to save aggressively, pay down debt quickly, build toward home ownership or other major financial goals, and absorb financial shocks without destabilisation. It is worth knowing that this margin can shrink quickly if your household changes — a new child, a partner leaving the workforce, or a move to a higher-cost county can each significantly raise your living wage threshold. Reassessing regularly is still valuable even from this position.

The Debt Complication — Why It Matters for This Assessment

The living wage does not include debt repayment of any kind. No student loan payments. No credit card minimums. No car loan payments beyond the operational cost of transportation. This is one of the most important limitations of using the living wage as a personal sufficiency benchmark — and it affects a huge portion of the working population.

If you carry debt, your true income requirement is higher than the living wage figure. The question is: by how much?

Your debt-adjusted income requirement

Living wage (annual) + Total annual debt payments = Your real minimum income need

Example:

Living wage: $52,000/year

Student loan: $4,800/year ($400/month)

Car loan: $3,600/year ($300/month)

Credit card minimum: $1,200/year ($100/month)

Real minimum: $52,000 + $9,600 = $61,600/year needed

In that example, the living wage says $52,000 is technically sufficient. But the actual minimum income needed to cover both basic expenses and existing debt obligations is closer to $62,000. A worker earning $56,000 — which looks like a $4,000 margin above the living wage — is actually $5,600 short of what they genuinely need.

This is why many people who technically earn above the living wage still feel financially trapped. The living wage does not see their debt. But their bank account does.

💡 What to do with this: Add your total annual debt payments to your living wage figure to find your real income floor — the number you genuinely need to earn to cover both basic expenses and existing obligations without accumulating new debt. Compare your actual income against this adjusted figure, not just the raw living wage.

If You Are Below the Living Wage — Honest Options

Finding out your income falls below the living wage for your household is not a pleasant result. But it is a useful one. It tells you that the financial stress you feel is not imagined or a result of bad habits — it has a structural cause. And structural problems, unlike character problems, have structural solutions.

There is no single answer that works for everyone. The right path depends on your industry, your household, your location, and your options. But here are the levers that actually move the number, roughly in order of impact.

Increase income — the highest-impact lever. A wage increase, a better-paying role, a second income in the household, or additional work hours are the most direct ways to close the gap. Use the living wage figure as your target when evaluating a raise request or a new job offer. Post 4 in this cluster covers how to use living wage data in salary negotiations specifically.

Reduce the largest cost categories. Housing is usually the biggest variable. Shared housing arrangements, a move to a lower-cost area within commuting range, or a roommate can meaningfully reduce the income required to cover basic costs. Transportation is the second largest opportunity — eliminating or downsizing a vehicle, or moving closer to transit, can free up several hundred dollars per month.

Check your eligibility for assistance programs. Depending on your income and household type, you may qualify for programs that directly offset living wage costs — SNAP for food, Medicaid or marketplace subsidies for healthcare, childcare assistance programs like CCAP or Head Start, or housing assistance. These programs exist precisely for the gap between what low-wage workers earn and what they need. There is no shame in using them while you work toward a more sustainable income level.

Pursue skills or credentials that move you to higher-paying work. Some income gaps are temporary — you are in an entry-level role or a training period that leads to significantly higher pay within a defined timeframe. If that path is clear and realistic, the short-term gap is manageable. If it is not clear, investing in skills, certifications, or credentials that open doors to better-compensated work is often the most durable solution available.

Reduce or restructure debt obligations. If debt payments are a significant portion of what pushes your real income requirement above your earnings, addressing the debt — through refinancing, income-driven repayment plans, or focused payoff — can reduce the gap over time even before your income increases.

⚠️ A realistic note: For people well below the living wage in high-cost cities, the gap can feel impossibly large. Some situations genuinely require more than one change simultaneously — a location move combined with a better-paying job, or an income increase combined with reduced housing costs. Be honest about what is realistically achievable in your specific circumstances, and prioritise the changes that have the largest impact on the gap.

If You Are Above the Living Wage — What to Focus on Next

Clearing the living wage threshold is a meaningful milestone. Your basic expenses are covered. The financial floor is under you. But the living wage is just the beginning of a financially secure life, not the destination. What you do with the margin above it determines whether you stay on solid ground or build something more durable.

🚨 Emergency fund first

If you do not have three to six months of essential expenses saved in a liquid, accessible account, this is the first priority. The living wage only covers you if your income continues uninterrupted. An emergency fund covers you when it doesn’t. Without one, you are one job loss, one illness, or one major repair away from falling below the living wage regardless of how well you are doing right now.

💳 High-interest debt next

Credit card debt and other high-interest obligations cost more in interest each month than most savings accounts return. Eliminating high-interest debt produces an immediate, guaranteed return equivalent to the interest rate — which is typically 18–25%. No investment reliably beats that. Once high-interest debt is gone, the monthly cash flow it consumed becomes available for savings and other goals.

🏦 Retirement contributions

Time is the most powerful variable in retirement savings. Even modest contributions started early compound significantly over a career. If your employer offers a retirement match, contribute at least enough to capture the full match — that is immediate 50–100% return on that portion of your savings. Beyond the match, the appropriate contribution level depends on your age and gap to retirement.

Once those three foundations are in place, you have the basis to think about longer-term goals — home ownership, further education, starting a business, or building wealth through investment. The living wage check tells you when the foundation is covered. Everything above it is the structure you build on top.

A new child, a move, a partner stopping work — each can shift your living wage requirement significantly. Re-run the MIT Living Wage Calculator any time your household situation changes to see exactly what the new figure looks like.

When to Run This Assessment Again

This is not a one-time exercise. The living wage changes as local costs change, and your household situation — and your income — changes over time. Running this assessment on a regular cycle, or whenever something significant shifts, keeps you oriented to reality rather than operating on stale assumptions.

📅 Run it annually

At minimum, revisit the assessment once a year — ideally around your annual performance review or when you receive any salary adjustment. The MIT calculator updates its county-level figures periodically as local costs change, so a living wage that was accurate 18 months ago may now be higher. What felt like a comfortable margin can erode silently as housing and childcare costs climb while wages stay flat.

🔄 Run it when your situation changes

Certain life events warrant an immediate reassessment: a new child or dependent joining the household, a partner entering or leaving the workforce, a significant change in your housing costs, a move to a different county, a job change with a different salary or benefits package, or the addition or elimination of a major debt obligation. Each of these can shift your living wage requirement or your effective hourly rate by several dollars an hour.

The goal is not to obsess over the number. It is to check in regularly enough that you know whether the direction of travel in your financial life is positive or negative — and to catch any drift below the living wage early, before it becomes entrenched.

The MIT Living Wage Calculator on Waldev is free, takes under a minute, and is updated with current cost-of-living data. Keep it accessible for your next annual review or life change.

Frequently Asked Questions

How do I know if I am earning a living wage?

Start by finding the living wage for your specific county and household type using the MIT Living Wage Calculator. Then convert your gross annual income to an hourly rate by dividing by 2,080. If your hourly rate equals or exceeds the living wage figure, you are at or above the threshold. If it falls short, there is a gap between what you earn and what basic expenses in your location require. The assessment in this guide walks you through each step in detail.

Does earning above minimum wage mean I earn a living wage?

Not automatically. The minimum wage is a legal floor set by legislation — it reflects what employers are required to pay, not what workers need to earn. The living wage is a separate calculation based on actual local costs. In many U.S. counties, the living wage is significantly higher than both the federal and state minimum wage. Earning above the minimum wage is a different question from earning a living wage.

What does it mean if I earn below the living wage?

It means your income, on its own, is technically insufficient to cover all basic living expenses in your location for your household type. In practice, people below the living wage typically manage through a second income in the household, government assistance programs, debt, reduced consumption, or shared housing. It is a structural problem, not a personal failing — and it has structural solutions. The “If You Are Below” section of this guide covers the most impactful options.

Should I include my partner’s income when checking against the living wage?

It depends on the household type you use. The MIT Living Wage Calculator has separate figures for one-worker and two-worker households. If both you and your partner work, use the two-adult, two-working figure and compare each person’s individual income against the per-person living wage for that configuration. If only one of you works, use the one-worker household figure and compare that single income against the full household living wage requirement — because one income must cover the entire household’s basic needs.

What if I have multiple income sources?

Add all gross income sources for the past 12 months — primary job, side work, freelance, rental income, or other regular earnings. Divide the total by 2,080 to get an effective hourly equivalent. Compare that against the living wage for your county and household type. If the combined total clears the living wage, your household income is technically sufficient at the basic needs level, even if individual income streams alone would not be. Use 12-month actuals, not projections, and be conservative.

The calculator says I earn enough, but I still feel financially stressed. Why?

Several reasons. First, the living wage is a bare-minimum benchmark — earning it means basic expenses are technically covered, not that you have financial breathing room or any cushion. Second, if you carry debt — student loans, credit card balances, a car loan — those payments are not included in the living wage but come directly out of your take-home pay, creating a real shortfall the calculator cannot see. Third, the model uses average local costs; your actual rent or healthcare expenses may be higher than the county median. The hidden gaps section of this guide covers each of these in detail.

How often should I check my income against the living wage?

At minimum, once a year — ideally timed with your annual performance review or salary adjustment. Also run it any time your household changes significantly: a new child, a partner entering or leaving the workforce, a move to a different county, or a major change in housing costs. The living wage itself changes as local costs change, so a figure that was accurate two years ago may now understate what you need.

The Assessment Is Worthless Without the Number

Everything in this guide depends on one starting point: the living wage figure for your specific county and your specific household type. Without that number, the rest of the assessment is just arithmetic in the abstract. With it, you get clarity about something most people deliberately avoid thinking about too precisely.

The MIT Living Wage Calculator is free, takes under a minute, and gives you a county-level, household-specific result based on real local cost data — not a national average, not a political estimate, but an economic calculation grounded in what things actually cost where you live.

Pull the number. Do the five steps. Write down your margin or your gap in annual dollars. Then decide what to do with what you find — armed with honesty rather than assumption.

The MIT Living Wage Calculator on Waldev is free, requires no account, and returns a county-specific result for your household type in under a minute. That is step one of everything else in this guide.

Dr. Amy Glasmeier’s research team maintains the county-level living wage methodology and data the calculator and this guide are built on.

The USDA’s regular food plan cost updates provide the food cost component of the living wage calculation — the basis for the grocery estimates used in the model.

The CFPB publishes accessible guides to budgeting, debt management, and financial planning that complement a living wage self-assessment with practical next steps.

Federal government resource for identifying assistance programs — food, healthcare, housing, childcare — for households earning below or near the living wage threshold.

Disclaimer: This article is for general informational and educational purposes only. The assessment framework and illustrative examples throughout are designed to help readers understand the living wage concept in relation to their personal income — they are not a substitute for professional financial advice. Living wage figures vary by county, household type, and year. Your actual cost of living may differ from the county averages used in the MIT model. If you are experiencing serious financial hardship, consider reaching out to a nonprofit credit counsellor or financial coach for personalised guidance. This article does not constitute financial, legal, or tax advice.