These two terms get tangled up constantly — in news headlines, job listings, political debates, and everyday conversations. Some of the confusion is innocent. Some of it is deliberate. Either way, the misconceptions have real consequences for people trying to figure out whether their paycheck is actually enough. This article goes through the seven most common myths, explains where each one comes from, and replaces it with something more accurate and useful.

What This Article Covers

Jump to any myth using the links below, or read straight through.

Why the Confusion Exists in the First Place

Before getting into the myths themselves, it is worth understanding why these two terms get mixed up so often. It is not because people are careless — it is because the terms sound like they should mean the same thing, and the policy debates around them use them almost interchangeably.

Think about how minimum wage is typically framed in public discussion. Politicians arguing for higher minimum wages routinely say things like “nobody who works full-time should live in poverty” or “workers deserve a wage they can live on.” That framing — deliberately or not — implies that the minimum wage either already is a living wage, or is close enough that closing the gap is simple. Neither is true in most of the country.

At the same time, the term “living wage” gets attached to everything from activist campaigns to corporate PR statements. When a large retailer announces a “$20 minimum wage,” that gets described in headlines as a “living wage commitment” — even when $20/hour falls short of the actual living wage for most families in the cities where those stores operate.

The result is a fog. Words that mean specific, different things get blurred until people stop being able to tell them apart. Let’s clear that up.

Once you understand the difference, the next step is comparing your income against the real figure for your area. The MIT Living Wage Calculator on Waldev gives you a county-level result in seconds.

“A living wage and a minimum wage are basically the same thing.”

They are built from completely different foundations — one is a legal rule, the other is an economic calculation.

The minimum wage is set by a vote. Congress passes a number, the President signs it, and that becomes the legal floor employers must pay. There is no automatic mechanism that connects the federal minimum wage to the actual cost of living in any city or county. The current federal minimum of $7.25 per hour has not changed since 2009 — more than fifteen years during which rents, food prices, healthcare costs, and childcare rates have all climbed substantially in most of the country.

The living wage is calculated the other way around. Researchers — most prominently Dr. Amy Glasmeier’s team at MIT — start with actual local costs: what does a 1-bedroom apartment rent for in this county? What does center-based childcare cost? What does a basic health plan cost? They add those numbers up, account for taxes, divide by annual work hours, and arrive at the hourly figure a worker would need to cover those costs without outside help.

These are fundamentally different processes. One is political; the other is economic. One changes when legislators act; the other changes when living costs change. They happen to use similar language — “wages” — which is where the confusion starts. But the underlying logic is completely different.

Set by law. Changed by legislative vote. The same rate applies to almost all workers in the jurisdiction regardless of where they live or how large their family is.

Calculated from real cost data. Changes when living costs change. Varies by county and by household type — a single adult and a single parent with two kids have very different living wages.

“If you earn above the minimum wage, you’re earning a living wage.”

Earning more than the minimum wage does not mean you’re earning enough to cover your actual costs.

This misconception follows logically from Myth #1. If you believe minimum wage and living wage are the same concept, then earning above the minimum wage would logically mean you’re above the living wage. But since they’re built from different foundations, that logic doesn’t hold.

Consider a concrete scenario. Suppose a worker in a major coastal city earns $18/hour — which is well above the federal minimum of $7.25 and even above most state minimums. That sounds like a comfortable buffer above the minimum, right? But if the living wage for a single adult in that specific county is $24/hour — which is not unusual in high-cost metros — then that $18/hour worker is still $6 short of what they need to cover basic expenses. They’re above the legal minimum. They’re not earning a living wage.

Now add a child to that household. The living wage for a single parent with one child in that same county might be $35–$40/hour once childcare costs are factored in. That same $18/hour wage doesn’t even cover half of what’s needed.

The gap between “above minimum wage” and “living wage” varies enormously by location and household size. In a low-cost rural county, a $15/hour wage might genuinely meet or slightly exceed the living wage for a single adult. In an expensive coastal city, even a $20/hour wage may fall short. The number that matters is not whether you beat the minimum — it is whether you meet the actual threshold for your specific location and family situation.

Before assuming your wage is sufficient, run it against the real local figure. The living wage calculator shows the county-level threshold for your exact household type.

“The living wage is a single national number — like the minimum wage.”

The living wage changes county by county, driven mostly by housing costs — and the variation is enormous.

This myth is surprisingly common even among people who understand the basic concept. They’ve heard that the living wage is something like “$20/hour” or “$18/hour” and treat that as a universal figure. But there is no universal living wage. The number that applies to you depends entirely on where you live.

The primary reason for this is housing. Rent is by far the biggest line item in any living wage calculation, and rents in the United States vary more dramatically than almost any other major consumer cost. A modest one-bedroom apartment in a rural Mississippi county might rent for $600/month. That same type of apartment in San Francisco, Boston, or Seattle might cost $2,800–$3,500/month or more. That single difference — roughly $2,200 per month — translates to over $26,000 in annual gross income difference, before a single other expense is changed.

Childcare costs add another layer of geographic variation. Some states have well-developed subsidized childcare infrastructure. Others have expensive, undersupplied markets. A county where center-based infant care costs $800/month requires a significantly lower living wage for families than one where the same care costs $1,800/month.

The MIT model calculates the living wage separately for every county in the United States. That granularity is the whole point. A statewide average living wage, let alone a national one, smooths out variations that are genuinely massive — and that actually matter when you’re deciding whether a job offer or a city is affordable for your family.

| Location type | Typical housing cost driver | Effect on living wage |

|---|---|---|

| Rural, low-cost county | Low rents, often under $800/mo for 1-bed | Living wage closer to $14–$17/hr for single adult |

| Mid-size inland city | Moderate rents, $900–$1,400/mo for 1-bed | Living wage typically $17–$21/hr for single adult |

| Major metro, non-coastal | Rents rising, $1,300–$1,800/mo for 1-bed | Living wage often $20–$24/hr for single adult |

| High-cost coastal metro | Rents frequently $2,200–$3,500+/mo for 1-bed | Living wage commonly $24–$30+/hr for single adult |

Note: These ranges are illustrative based on general cost-of-living patterns. Actual figures depend on your specific county and household type.

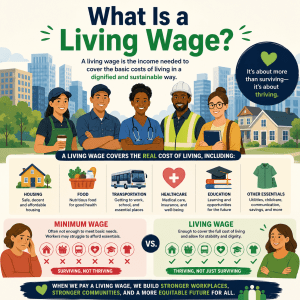

“If you’re earning the living wage, you’re living comfortably.”

The living wage is a survival floor, not a comfortable income. Earning it means your bills are covered — nothing more.

This is probably the most emotionally loaded misconception on the list. The word “living” sounds positive. It sounds like it describes a decent life. So people assume that earning the living wage means you’re doing reasonably well.

You’re not. You’re scraping by.

The living wage, as calculated by the MIT model, covers rent, groceries, basic transportation, a basic health plan, and childcare if you have kids. That’s it. There is no savings contribution built in. No emergency fund. No retirement account. No vacation. No debt repayment. No college fund. No discretionary spending beyond the narrowest personal care basics.

A worker earning exactly their local living wage has their basic expenses covered — but they’re one car breakdown, one unexpected medical bill, or one month of reduced hours away from serious financial trouble. There’s no buffer. There’s no margin. The bills get paid and that’s the ceiling.

Personal finance researchers sometimes talk about three tiers above the poverty line. The living wage sits at the bottom tier — what some call the “survival wage.” Above that sits a “stability wage” that adds modest savings and debt repayment. Above that is a “thriving wage” that allows for real discretionary spending, retirement contributions, and genuine financial security. The living wage gets you to tier one. Most people want to reach tier two or three.

Understanding this distinction matters practically. If someone tells you that a job offer is “above the living wage” and frames that as a strong selling point, it’s worth probing further. How far above? Does it include any meaningful margin for savings or unexpected costs? Being slightly above the living wage in a high-cost city is not the same as financial comfort.

What the living wage covers: Rent, groceries, basic transportation, healthcare premiums, childcare (if applicable), basic personal care, and gross taxes on those expenses.

What the living wage does NOT cover: Emergency savings, retirement contributions, debt repayment, eating out, entertainment, vacations, home ownership, life insurance, or any significant financial cushion.

What “comfortable” actually requires: Most financial planners suggest that genuine financial stability requires earning noticeably above your local living wage — enough to save at least 10–15% of income, maintain an emergency fund, and service any debt obligations.

“If we just raise the minimum wage high enough, everyone will automatically earn a living wage.”

A single national minimum wage cannot solve a problem that varies dramatically by location and household size.

This misconception lives in political debates more than personal finance conversations, but it affects how people think about their own wages and what to expect from policy changes. The argument sounds logical: if the minimum wage is too low, just raise it to the living wage level and the problem is solved. But the math doesn’t work that way.

The living wage is not a fixed number. It varies — as we’ve covered in Myth #3 — by county and by household. A single national minimum wage of, say, $20/hour would be generous in a rural county where the living wage for a single adult is $15/hour. That same $20 would still fall well short in a major coastal city where a single adult needs $26/hour, and it would be deeply insufficient for a single parent with two children in that same city who may need $38–$42/hour or more.

There is no single number that simultaneously satisfies the living wage threshold for a childless single adult in rural Alabama and a single parent of two children in Seattle. These are genuinely different economic situations in genuinely different cost environments.

This is not an argument against minimum wage increases — higher minimums do help low-wage workers in most scenarios. It is an argument for being precise about what a minimum wage increase can and cannot accomplish. Describing any specific minimum wage as “the living wage” oversimplifies a problem that is inherently local and household-specific.

💡 What actually works at the household level: Knowing your specific county’s living wage for your household type — and comparing it to your actual income — is far more useful than tracking national political figures. The living wage calculator gives you that county-specific answer in about 30 seconds.

“The living wage only matters if you’re a low-income worker.”

The living wage is a useful benchmark for anyone evaluating income sufficiency — including middle-income earners considering moves, career changes, or family expansion.

There’s a tendency to treat the living wage as a concept that only concerns workers at the bottom of the pay scale — minimum wage earners, service industry workers, people who need government assistance. If you earn a salary, the thinking goes, this doesn’t apply to you.

That’s too narrow a view. The living wage is useful as a baseline benchmark in several situations that affect people at many income levels.

Relocating to a new city

Someone earning $65,000/year in a mid-cost city who accepts a $70,000 offer in San Francisco might assume it’s an upgrade. But if the living wage for their household type in that new city is $85,000+, they’ve actually moved into a more financially strained position despite a nominal raise.

Having children

A dual-income household comfortably above the living wage for two childless adults may find themselves below the living wage for their new household type once a child arrives and one partner reduces hours or leaves the workforce temporarily.

Evaluating a job offer

A new graduate evaluating competing offers can use the living wage as a sanity check — does this salary actually cover life in this city, for my household size? It’s a more grounded question than just comparing offer amounts.

Career transitions

Someone leaving a high-paying job to pursue a passion project, change industries, or start a business can use the living wage as the floor for what they need to earn during the transition to stay financially stable.

The living wage is not just a measure of poverty. It’s a measure of adequacy. Anyone can use it to ask: is this income actually enough for this household, in this place, right now?

“Employers are legally required to pay the living wage.”

There is no federal living wage law. Most employers have no legal obligation to pay it — only to meet the applicable minimum wage.

This misconception runs in both directions. Some workers assume they are entitled to a living wage and are surprised to discover that their employer has no such legal obligation. Some employers, on the other hand, think they’re already compliant with a “living wage requirement” simply by paying minimum wage.

The legal landscape is this: the federal minimum wage ($7.25/hour as of this writing) is the legal floor for most workers in the United States. States may set higher minimums, and some do — California, Washington, and New York, for example, have state minimums substantially above the federal level. Workers are entitled to whichever is higher: the federal minimum or their applicable state minimum.

The living wage is not a federal law. It is a research-based benchmark with no mandatory legal force. There are exceptions:

More than 100 U.S. cities and counties have passed living wage ordinances. These typically require businesses that hold contracts with local government — construction, cleaning services, food service at public facilities — to pay workers above a locally defined living wage. They generally do not apply to private employers with no government contracts.

Some private employers — particularly large corporations under public scrutiny — have voluntarily committed to paying above a certain hourly floor described as a “living wage.” These commitments are self-defined and not legally binding in the way that minimum wage laws are. A company can retract them, adjust them, or apply them selectively.

Some nonprofit and industry organizations offer “living wage employer” certification for companies that voluntarily meet or exceed the living wage for their location. Participation is optional, and standards vary by certifying organization.

The practical upshot for workers: knowing the living wage for your area is genuinely useful — but you cannot assume your employer is legally required to pay it. The right use of this information is personal financial awareness, not a legal claim against an employer.

⚠️ Important: If you believe your employer is paying you below the applicable minimum wage (federal or state), that is a legal matter worth pursuing through the Department of Labor’s Wage and Hour Division. Falling below the living wage, on the other hand, is not automatically illegal — though it is an important financial signal worth taking seriously.

Side-by-Side: What Each Term Actually Means

If you want to keep these two concepts straight going forward, this table is the cleanest reference. The differences are not subtle once you know what to look for.

| Question | Minimum Wage | Living Wage |

|---|---|---|

| What is it? | The lowest pay an employer can legally offer | The calculated income needed to cover basic necessities |

| Who sets it? | Federal government, state governments, or both | Researchers using real cost-of-living data (e.g., MIT) |

| Is it legally required? | Yes — employers must meet it or face penalties | No — except under some local ordinances |

| Is it the same nationwide? | Federal floor is flat; states vary above that | Varies by county — sometimes by a factor of 2× |

| Does family size affect it? | No — one rate for all workers regardless of dependents | Yes — calculated separately for each household type |

| Does it keep up with inflation? | Only when legislators vote to change it | Yes — MIT model updates regularly with current data |

| Does it include savings? | N/A — it is just a wage floor | No — covers necessities only, not savings or debt |

| Can I use it to plan a budget? | As a legal minimum, not a planning target | Yes — as a floor for what your household needs to earn |

Once you have a clear picture of the difference, the most useful next step is finding the actual living wage figure for your location. Use the free MIT Living Wage Calculator on Waldev to look up the number that applies to your county and household type.

How to Check Your Own Situation in 3 Steps

Now that the misconceptions are out of the way, here’s the practical question: how do you apply this to your own life? The process is simpler than most people expect.

Start with the MIT Living Wage Calculator on Waldev. Select your state, then your county, then your household composition — how many adults, how many are working, how many children. The calculator returns an hourly living wage figure based on current local cost data. This is your baseline number.

Take your annual salary or total annual income and divide by 2,080 (the number of hours in a standard full-time working year — 40 hours × 52 weeks). If you work part-time or multiple jobs, account for actual hours worked. The result is your gross hourly equivalent, which you can compare directly against the living wage figure.

If you’re below the living wage threshold for your household type: your income may not be covering all basic expenses without some form of assistance, additional income, or debt. If you’re at or just above it: your necessities are technically covered, but there is little room for savings, emergencies, or anything beyond basics. If you’re meaningfully above it: you have the margin to start building genuine financial stability. The further above, the more room you have to save, plan, and manage unexpected costs.

💡 Tip: Run this check again any time your household situation changes — a new child, a move to a different city, a partner joining or leaving the workforce. The living wage for your household can change significantly with each of those events, and it’s worth knowing where you stand.

Frequently Asked Questions

Is minimum wage the same as a living wage?

No. Minimum wage is the legally required pay floor set by legislation. A living wage is a research-based calculation of what a worker actually needs to cover basic costs in their location. In most U.S. counties, the living wage is significantly higher than the minimum wage — often by several dollars per hour, and sometimes by far more for households with children.

Does earning above minimum wage mean you earn a living wage?

Not automatically. Many workers earn above the minimum wage but still fall short of the living wage for their household type and location. A $15/hour or $18/hour wage may exceed the living wage in a low-cost rural county but fall well short in a major metro area — especially for households with children. The only way to know is to compare your actual wage against the county-specific living wage figure for your household type.

Is the living wage the same everywhere in the United States?

No. The living wage changes county by county. It is driven primarily by local housing costs, which vary enormously across the U.S. A single adult in a low-cost rural area may have a living wage of around $14–$16/hour, while the same household type in a high-cost coastal metro may need $24–$30/hour or more. For accurate local figures, use the MIT Living Wage Calculator.

Does a living wage mean you can live comfortably?

No. A living wage is a survival-level benchmark that covers basic necessities only — rent, groceries, basic transportation, healthcare, and childcare. It does not include retirement savings, an emergency fund, debt repayment, vacations, or meaningful discretionary spending. Earning the living wage means your basic bills are covered, not that you’re financially comfortable or secure.

Does raising the minimum wage automatically give everyone a living wage?

No. Because the living wage varies significantly by location and household type, no single national number can simultaneously satisfy the living wage threshold for all workers in all situations. A $20 federal minimum would exceed the living wage in many lower-cost counties but still fall short in expensive cities — especially for households with children. A blanket raise helps, but it cannot solve what is inherently a local, household-specific problem.

How do I find out what the living wage is in my area?

The most reliable and accessible source is the MIT Living Wage Calculator, available for free through Waldev’s MIT Living Wage Calculator page. You can look up any U.S. county, select your household type, and get a current hourly living wage estimate based on real local cost data.

Can an employer legally pay below the living wage?

Yes, in most cases. The living wage is not a federal law. Employers must meet the federal minimum wage or their applicable state minimum, whichever is higher. They have no legal obligation to meet the living wage threshold unless they are subject to a local living wage ordinance, which typically applies only to government contractors in the cities and counties that have passed such laws.

Seven Myths Down — One Honest Number to Go

The whole point of clearing up these misconceptions is to get you to a more accurate picture of your own financial situation. National headlines and political talking points will keep blurring these terms. You don’t have to let them blur your own thinking.

The living wage for your county and your household type is a real, calculable number. It’s not an opinion, it’s not a political position, and it doesn’t depend on what Congress last voted on. It’s based on what things actually cost where you live, right now.

Once you know that number, you can compare it honestly against what you earn, decide whether a job offer makes sense for your life, plan a realistic budget, or evaluate whether a proposed move to a new city genuinely improves your situation.

The MIT Living Wage Calculator on Waldev looks up the county-level living wage for your exact household type in seconds. It’s the fastest way to move from confusion to clarity about what you actually need to earn.

Dr. Amy Glasmeier’s research team maintains the county-level living wage methodology used as the basis for the calculator and the figures discussed throughout this article.

The Wage and Hour Division maintains the official federal and state minimum wage data used to establish the legal pay floors referenced in this article.

EPI publishes regular research on the gap between minimum wages and actual living costs across U.S. metro areas, a useful companion to the MIT model.

NLIHC’s annual “Out of Reach” report documents the gap between local wages and the income needed to afford housing, a key component of any living wage calculation.

Disclaimer: This article is for general educational and informational purposes only. The wage ranges and cost-of-living examples used throughout are illustrative and do not represent specific figures for any particular county or household. Living wage and minimum wage figures change over time. For current, location-specific data, consult the MIT Living Wage Calculator and official government sources. This article does not constitute financial, legal, or employment advice.